Why Do Auction Shipping Quotes Feel So Inconsistent? Because There Are Two Markets, Not One

Auction shipping quotes feel inconsistent because there are two freight markets, not one. Here's how to tell them apart and budget transport accurately.

Auction transport is not one market.

The dealership operations director who budgets whole-car auction buying with predictable per-unit freight costs, then gets a quote from a Copart yard that's 40 percent higher, is not dealing with an irrational carrier. The fleet coordinator watching a won vehicle accumulate storage fees while no carrier accepts the load is not the victim of a bad quote. Both are crossing from one freight market into another without realizing it.

A 9-car stinger hauler pulling an off-lease sedan from a Manheim sale and a wedge-trailer owner-operator winching a flooded Honda out of a Copart lot are technically both "auction transport carriers." Economically, they operate in different industries — different equipment, different pricing mechanics, different risk profiles. Most budgeting failures in auction transport trace back to treating them as one.

In this article, we walk through how the two markets actually work, why non-running vehicles carry the surcharges they do, and how dealers who occasionally cross between them can avoid the operational traps that sit at the boundary.

Whole-car auction freight and salvage auction freight share almost nothing operationally except the word "auction." The confusion between them is the most common source of budgeting failure we see, and naming the structural difference is the foundation for everything else in this article.

The first market is whole-car auction freight. This is the freight moving vehicles that sold at Manheim, ADESA, ACV Auctions, OVE, OEM (Original Equipment Manufacturer — the vehicle makers) closed sales, and dealer-to-dealer auctions. Cargo here is operational — the vehicles drive on and off trailers under their own power. Vehicle condition is standardized enough that a carrier can plan equipment, routes, and per-unit loading time with reasonable accuracy. Dealer buyers typically have established carrier relationships, and freight is often arranged through account-managed channels rather than spot-market load boards.

The second market is salvage auction freight. This is the freight moving vehicles that sold at Copart and Insurance Auto Auctions (IAA — the salvage arm of RB Global since the Ritchie Bros. acquisition in 2023). These vehicles are insurance total-loss units, catastrophe-damaged inventory, flood vehicles, burned-out frames, and collision wrecks. Cargo condition is highly variable. Much of it is non-running. Pickup and loading require specialized equipment that whole-car carriers do not operate. Pricing happens in a fragmented spot market where every buyer arranges transport independently.

These two markets share physical geography — Copart yards and Manheim sales sometimes sit in the same metro region — the general business of moving vehicles, and the word "auction." That is where the overlap ends. The carriers do not overlap. The equipment does not overlap. The pricing mechanics do not overlap. The typical transit times do not overlap. The risk profiles do not overlap.

This is our position on the topic: auction transport is not a single service category. Treating it as one produces the budget surprises, missed storage deadlines, dry-run fees, and "why is this quote so expensive" conversations that make auction logistics feel inconsistent. The cure is to identify which market a given vehicle sits in before the bid, and to plan transport according to that market's economics rather than the other one's.

The rest of this article breaks down what each market actually looks like and what it costs to operate in each.

How pickup works on a 9-car stinger

At a whole-car auction sale, our driver arrives, presents gate paperwork, and locates the vehicles assigned to the load. The cars drive on under their own power, up the stinger-steered trailer ramps and into position on the upper and lower decks. An experienced driver loading nine drive-on vehicles from a single auction location typically spends 2 to 4 hours from gate-in to gate-out, depending on vehicle placement in the yard and how busy the gate flow is that day.

Pickup operates on arrival-window flexibility rather than rigid appointment slots. A carrier running a multi-stop day can absorb a 30-minute delay at one stop without collapsing the rest of the route. There is no PIN-coded release system. There is no virtual queue fighting for a forklift. The trailer's hydraulic ramps are rated for rolling loads, the upper deck is designed for standard vehicle dimensions, and over-the-tire tie-down straps take a trained driver a few minutes per vehicle.

Drive-on loading is also safer for the cargo. A driver steering a functional vehicle up a ramp has full control over the car. The risks of secondary damage — bent suspension, torn floor pans, crushed exhaust components — that dominate non-running salvage loading simply do not exist in whole-car pickup.

Why this freight can be planned

The combination of standardized cargo, flexible pickup windows, and predictable loading times makes whole-car auction freight fundamentally plannable. Our Illinois–South Florida corridor, as one example, runs a reliable 4-day transit because the freight profile — drive-on vehicles on 9-car stingers out of established auction locations — supports planned routing and consistent lane execution.

Account-managed carriers (us included) typically serve whole-car auction work through dedicated account management rather than Central Dispatch load-board bidding. Our dealership clients work with a named point of contact, not a rotating dispatch queue. They get real-time tracking from origin to destination, timestamped photo documentation at pickup and delivery, and advance visibility on ETAs (estimated times of arrival). That operational posture is possible because the underlying freight profile is predictable enough to sustain it.

On who pays: the structure varies by account, but most of the time the dealer who bought the vehicle pays the freight. What matters structurally is not who pays but how the transaction is organized. In whole-car auction work, freight is usually arranged through an existing carrier relationship — not posted to an open marketplace for whichever hotshot carrier happens to accept it first.

The problem most dealership buyers face is wanting this kind of predictability on every auction transport they book. The struggle is that they occasionally buy from yards where this predictability structurally cannot exist. The resolution is to recognize that whole-car auction freight is plannable because of its structural properties — and not to assume that predictability carries over when they cross into the salvage market.

The infrastructure is real — and structurally different

Copart and IAA represent one of the largest concentrated freight origination networks in North American logistics. Copart operates more than 250 locations globally, with over 220 in North America, and sold more than 4 million units in its most recent fiscal year, according to its 2025 CEO letter to stockholders. The company owns more than 21,000 acres of land globally, with over 90 percent of it owned outright rather than leased. IAA adds roughly 200 U.S. facilities and processes approximately 2.5 million low-value, damaged, and total-loss vehicles annually, according to its published corporate information. Combined, the two networks handle roughly 80 percent of U.S. salvage auction volume.

This is infrastructure-grade density. But the carrier ecosystem serving it looks nothing like the one serving whole-car auctions.

Why the carrier economics are different

Salvage cargo is heterogeneous. A single Copart yard on any given morning holds flood-totaled sedans with seized brakes, collision vehicles with destroyed steering geometry, burned-out frames, pickups with missing wheels, and structurally compromised SUVs. A standard 9-car stinger trailer cannot safely load this cargo — the hydraulic ramps and tight upper-deck clearances assume the vehicle can be driven on under its own power and steered into position.

The workhorse equipment for salvage freight is therefore different: 3-to-4 car wedge trailers pulled by medium-duty Class 5 and Class 6 trucks, and single-vehicle flatbed rollbacks. These configurations offer continuous flat decks compatible with winching, lower loading angles, and tie-down access appropriate for dead vehicles. They sacrifice total payload capacity — three or four cars instead of nine — in exchange for the flexibility the cargo requires.

The supply base is also different. Because capital costs for a Class 5 truck and wedge trailer are far lower than for a 9-car stinger, the salvage freight market is dominated by independent hotshot owner-operators rather than corporate carriers. Fleet sizes of one to three trucks are the norm. Pricing happens on Central Dispatch, the dominant open load board in U.S. vehicle transport, which Cox Automotive reports facilitated more than 14 million vehicle moves in 2024 with over 20,000 carriers active over the prior year.

There is one more structural factor that compresses domestic carrier density further: export bifurcation. Copart's own 2025 CEO letter discloses that international buyers purchase approximately 40 percent of vehicles sold through U.S. auctions and account for nearly half of gross transaction value. Those vehicles do not enter the domestic over-the-road carrier market at all — they move to port-adjacent container stuffing facilities for export to Georgia, the United Arab Emirates, Germany, and other destinations. Roughly four in ten vehicles leaving a Copart yard are already committed to a parallel freight system before any domestic hauler sees them on a load board.

A note on our scope

We should name the boundary clearly. GB Cargo does not operate in the non-running salvage freight market. Our trailers are built for drive-on cargo, and we invest in new equipment designed around that profile. If a vehicle is damaged but still drives, we can move it. If a yard has forklift capacity and can load the vehicle directly onto one of our trailers, we can accommodate that too. What we do not do is winch-load inoperable salvage units onto specialized wedge trailers or rollbacks. That work belongs to carriers built around it — different equipment, different insurance, different operational DNA.

Naming this matters because the article's thesis — two markets, not one — also tells our clients something real about carrier selection. Not every carrier serves both markets, and the honest answer for dealers crossing between them is often that they need two carrier relationships, not one.

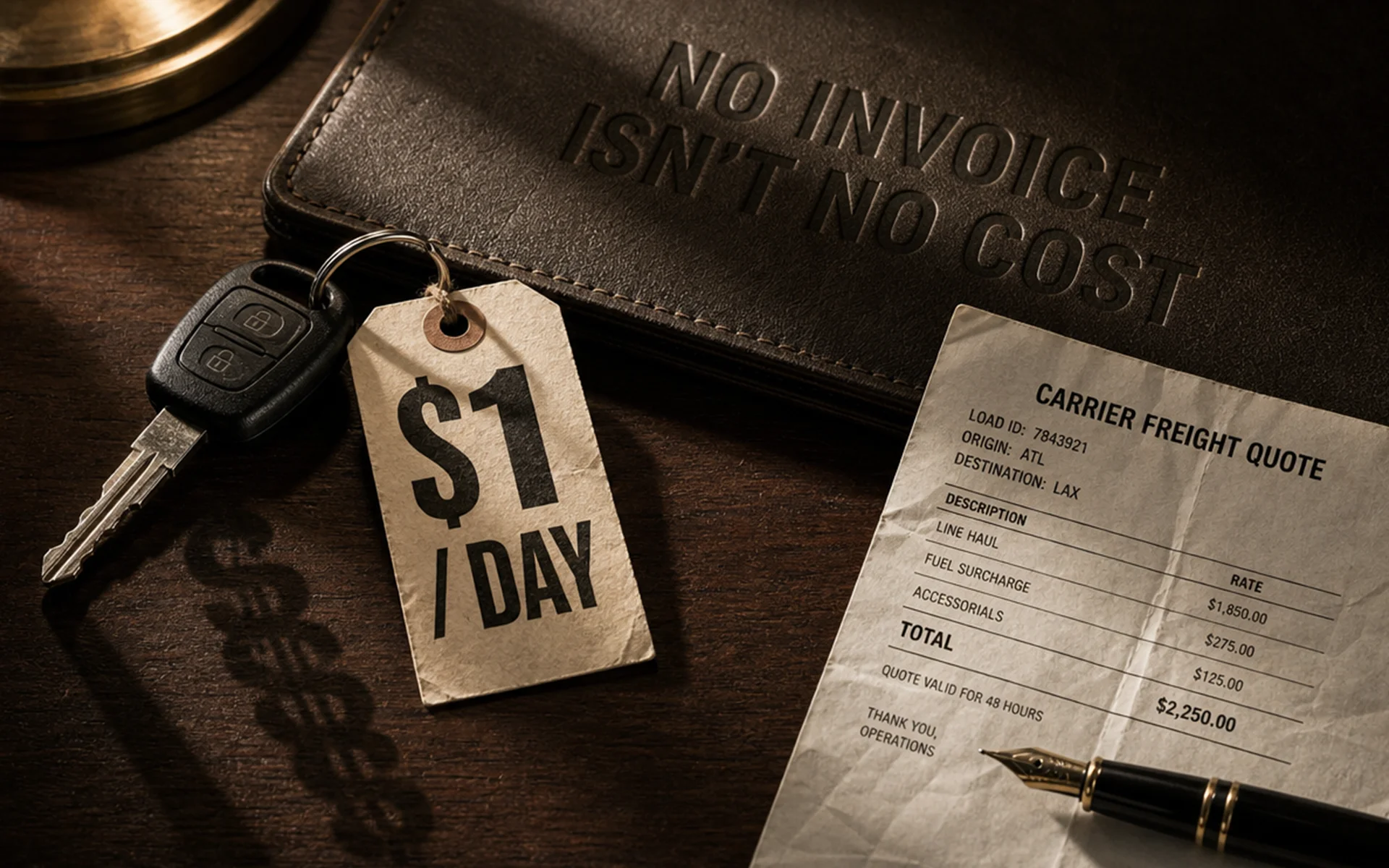

Buyers seeing a $150–$500+ surcharge on a non-running vehicle from Copart or IAA almost universally read it as carrier padding. They shop aggressively for the lowest quote — and frequently produce one of two outcomes. Either a dry run, where the carrier arrives without the right equipment, or a vehicle that sits in the yard for days while storage fees compound because no competent carrier will accept a sub-market rate.

The surcharge is not arbitrary. It is a stack of six real cost components, and understanding each one explains why the mechanical floor is what it is.

The practical takeaway: the non-runner surcharge has a mechanical floor set by these six components. Aggressive shopping produces one of two outcomes — a genuinely efficient specialized carrier at a fair rate, or a carrier who underquoted and will recoup the difference through fees, delays, or secondary damage claims. Buyers who do not understand this commonly end up paying more, not less.

Industry analysts sometimes describe Copart's yard network as the "Amazon of salvage" or compare it to an e-commerce fulfillment network. For a strategic analyst modeling Copart's macro advantages, the analogy is useful. For an auction buyer trying to plan transport, it is often misleading.

Where the analogy holds:

Where the analogy breaks:

The honest verdict: the analogy explains why carriers cluster around these yards at all. It does not explain what an auction buyer's freight experience will actually feel like. Expecting Amazon-grade reliability on a Copart pickup is how buyers get blindsided.

Most of the time, whole-car auction buyers and salvage auction buyers are distinct populations. Larger dealerships and fleet operators tend to stay inside whole-car inventory. Salvage buying is dominated by dismantlers, rebuilders, exporters, and small-to-mid dealers who have in-house repair capability.

The crossover scenario we see most often is the small-to-mid dealership with its own repair shop. The dealer spots a repairable Copart unit that fits a retail niche — a collision car they can fix and flip, or a specific model with hard-to-source parts availability. They win the auction and call the carrier they always use for their Manheim freight.

This is where the two markets collide operationally. Sometimes the regular carrier can handle it — if the vehicle is drive-on, or if the yard will forklift-load onto a standard trailer. Often they cannot. The dealer then scrambles for a specialized operator while the storage clock runs against Copart's 3-day free window (IAA's runs 4 business days). Every day of delay eats margin, and the promised retail price on the rebuilt vehicle starts to evaporate in logistics overhead.

Here is what we recommend to dealers working this crossover:

The crossover pattern is manageable when the buyer understands which freight market the specific vehicle sits in. It becomes expensive when they don't.

We built GB Cargo around the whole-car side of the auction transport market. Our fleet is new, drive-on, and designed for planned lane execution rather than spot-market improvisation. Our Illinois–South Florida corridor runs a reliable 4-day transit. Our 9-car haulers typically load in 2 to 4 hours at a single auction location with an experienced driver.

Our dealership clients work with a named account manager rather than a rotating dispatch queue. They see real-time tracking from pickup to delivery, with timestamped photo documentation at both ends.

We move running vehicles and damaged vehicles that can still be driven. We do not winch non-running salvage freight. That work belongs to specialized carriers — and knowing the difference is what this article is about.

Can GB Cargo transport non-running salvage vehicles from Copart or IAA?

We do not winch-load inoperable vehicles. If a vehicle is damaged but still drives, we can typically move it. If the yard has forklift capacity and can load the vehicle directly onto one of our trailers, we can accommodate that as well. For fully inoperable salvage freight that requires winching, specialized carriers with wedge trailers or rollbacks are the right fit.

Why does shipping a vehicle from a Copart yard sometimes cost more than the equivalent distance from a Manheim sale?

Because salvage and whole-car auction freight operate in two different markets with different equipment, different pricing mechanics, and different risk profiles. Salvage freight moves on smaller trailers with higher per-unit labor cost, runs on rigid appointment systems that create deadhead risk for carriers, and absorbs dry-run exposure priced into every quote. The distance is similar. The freight economics are not.

How long does it typically take to load a 9-car hauler at a whole-car auction?

In our experience, 2 to 4 hours for an experienced driver loading nine drive-on vehicles from a single auction location. Variability comes from where the vehicles are staged, how busy the gate is, and documentation flow.

When should a dealer avoid using their primary whole-car auction carrier for a Copart or IAA purchase?

Any time the vehicle is listed In-Op or requires winch loading. Whole-car carriers are built around drive-on cargo — their trailers, their insurance, and their loading workflow all assume it. Attempting to stretch that capability onto non-running salvage freight produces dry runs, secondary damage risk, and storage fee overruns. The better answer is to identify which market the vehicle sits in before the bid and choose the carrier accordingly.

Auction transport is not a single service category. It is two structurally different freight markets — whole-car and salvage — that share a word and almost nothing else operationally. The carriers, the equipment, the pricing mechanics, and the risk profiles diverge from the moment a vehicle hits the auction block.

Budgeting failures, storage fee surprises, dry runs, and "why is this quote so expensive" conversations almost always trace back to treating these two markets as one. The resolution is structural: identify which market a given vehicle sits in before the bid, plan transport around the economics of that market, and choose a carrier built for it.

Quotes that feel inconsistent usually aren't. They are accurately priced reflections of two different freight markets, and recognizing that is the foundation of a working auction transport budget.

Before your next auction purchase, take two minutes to place the vehicle in the right freight market. Is it a drive-on vehicle from Manheim, ADESA, or an OEM closed sale, heading to a dealership through a planned lane? That is whole-car freight — predictable, plannable, typically account-managed. Is it an In-Op or condition-variable unit from a salvage auction? That is salvage freight — specialized equipment, spot-market pricing, different rules entirely.

If your business runs consistent whole-car auction lanes and you want a carrier relationship built around planned execution, dedicated account management, and real-time tracking, talk through your specific corridor with us.

Stay informed on the latest news and insights from GB Cargo.