Is a $1-a-Day Relocation Rental Actually Cheaper Than a Carrier?

A $1-a-day relocation rental rarely beats a carrier once you count foregone revenue and mileage. See the break-even math that decides reposition or haul.

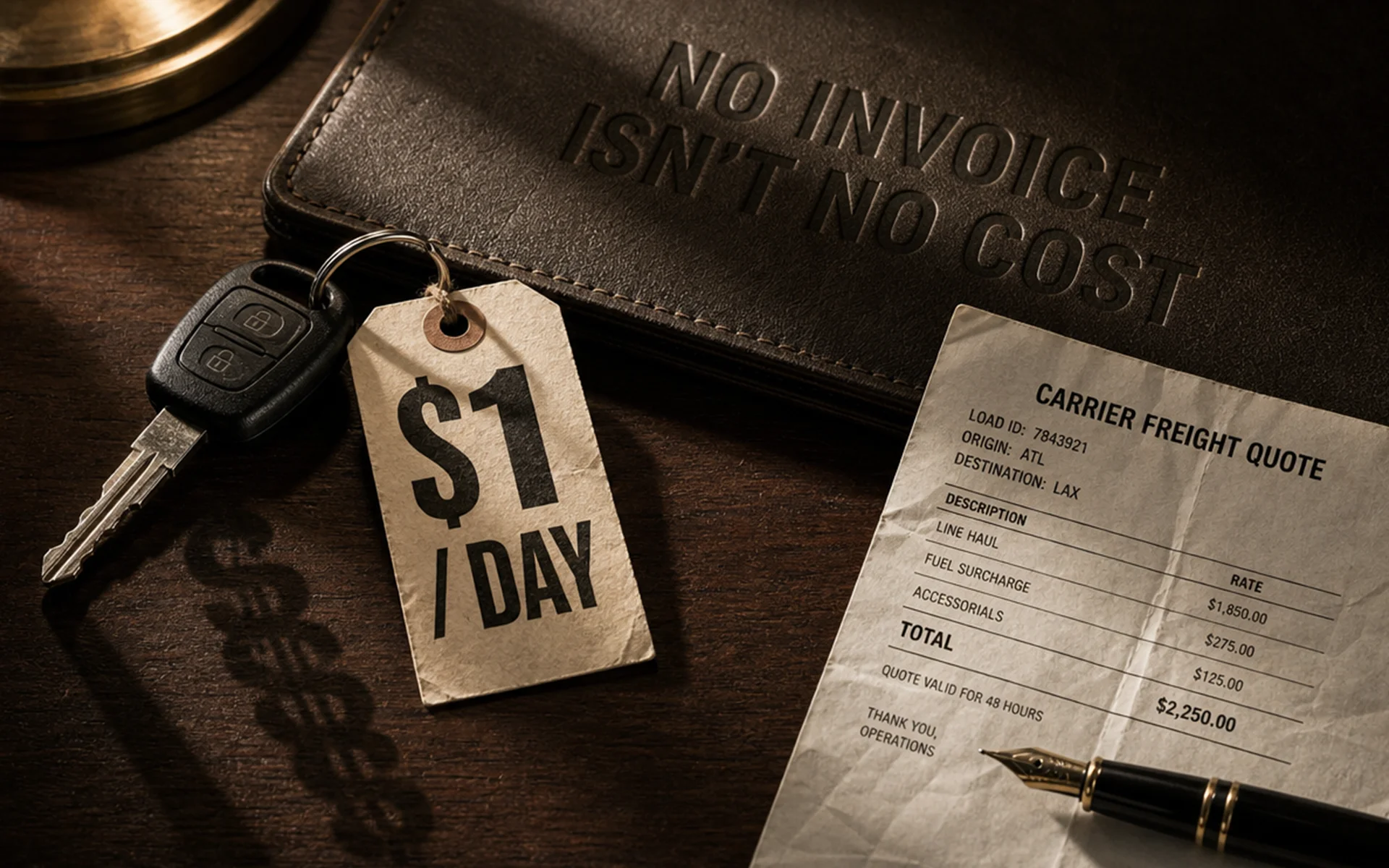

A relocation rental priced at $1 a day is never a $1-a-day decision.

When you move a sedan from Chicago to Miami on a deeply discounted one-way rate, the transit doesn’t cost you $5. It costs the rental revenue that car didn’t earn while it sat on the road, plus the mileage it burned getting there — often $300 to $500 or more per vehicle. None of that lands as an invoice, so it rarely gets weighed against the carrier quote it supposedly beat.

Here’s the part most fleet teams miss: the reposition-or-haul decision doesn’t turn on the rate at all. It turns on one number that few operators track at the location level — origin utilization. Move that number from 65% to 90% on the same lane, and the cheaper option flips.

Vehicles follow customers, not return lanes. Every one-way transaction redistributes inventory across your network, and often in the direction that deepens an imbalance rather than fixing it. This is the structural problem at the center of car rental fleet operations: a customer picks up in Chicago and drops in Miami, you earn the revenue, but now you hold one fewer car in Chicago and one more in Miami — whether or not Miami needed it. Multiply that across thousands of daily transactions and the drift becomes continuous, not episodic.

The cost of that drift is larger than it looks, because a vehicle in transit is also a vehicle removed from rentable inventory. At a national operator running hundreds of thousands of units at roughly 70% utilization, even modest displacement across markets adds up to real revenue lost while cars travel between locations. The repositioning bill is never just the cost of the move; it’s the move plus the earning days the vehicle gives up along the way.

The good news is that most of this imbalance isn’t random. It follows a calendar you can read in advance.

Three patterns drive most of the management problem. Seasonal one-directional drift is the most predictable: snowbird corridors, summer resort markets, ski-season peaks. Event-driven surges — major sporting events, conventions, hurricane evacuations — come with shorter lead times and are harder to pre-position for. And structural location-type imbalance runs continuously, as airports absorb one-way leisure drop-offs while downtown and neighborhood branches run short.

The snowbird corridor is the clearest case, and it’s one we run constantly. From October through January, southbound demand from the Midwest and Northeast toward Florida surges — lane data puts the southbound increase at roughly 40%. Our own Illinois-to-South Florida lane reflects exactly this pattern: heavy southbound volume in the fall, then a reversal in spring as the same vehicles, and the snowbirds, head north.

That reversal matters for budgeting. A lane that’s expensive to haul southbound in November is expensive to haul northbound in April, because the carrier is now fighting the deadhead in the opposite direction. The imbalance never disappears; it just changes direction with the season.

The operators who get hurt are the ones who treat this as a surprise. Reactive repositioning happens at exactly the moment when both hauling capacity and rentable vehicles are scarcest — which is the most expensive moment to act.

Once you accept that the drift is coming, you have two real tools to correct it.

The first is the relocation rental: a deeply discounted one-way rate that converts an asset-movement cost into partial revenue. If a car needs to move from a surplus location to a shortage location, and a traveler wants to make that same trip, a steep discount gets the vehicle repositioned while collecting some revenue instead of pure expense. Major operators use this as an active demand-shaping tool — pricing one-way moves up or down depending on whether the direction helps or hurts their inventory position.

The second is carrier hauling: contracting a professional auto transporter to move the vehicles physically, on a schedule, with a defined pickup and delivery window.

Neither is universally cheaper, and that’s the whole point. They have fundamentally different cost shapes. A relocation rental has a low or near-zero cash outlay but high implicit costs that never reach a statement. Carrier hauling has a high, visible cash outlay but near-zero implicit cost. The mistake is comparing the visible number on one against the visible number on the other — because one of those options keeps most of its cost out of sight.

Operators reach for relocation rentals because they need to move idle inventory cheaply, and a $1/day rate looks unbeatable. The problem is that the comparison is rigged from the start: the relocation rental wins by default because its real costs are invisible, while the carrier’s cost arrives as a quote you can’t ignore.

So let’s make the invisible costs visible. There are four.

Foregone revenue is the biggest one. This is the difference between the relocation rate you offered and what that vehicle would have earned in the destination market once it arrived. Price a car at $1/day for a 5-day transit and the nominal revenue is $5. But if that same car had been earning at the industry’s recent revenue-per-day — around $55 at one major operator — across those five days, it would have generated roughly $278 at full utilization. Adjust for realistic utilization in the 70–79% range and the foregone revenue is roughly $195 to $220 for that one 5-day window. The relocation rental didn’t cost $5. It cost what the car didn’t earn.

That figure swings hard on one thing: how busy the origin location actually is. Operators target 70–85% fleet utilization. Below that line, an idle day costs almost nothing at the margin — the car’s fixed daily cost runs whether it moves or sits, so a vehicle that would have been idle anyway carries near-zero opportunity cost in transit. Above that line, every unit you remove from available inventory has immediate revenue impact, because demand exists to absorb it. A relocation rental drawn from a genuinely surplus location is close to free; the same move pulled from a balanced or short location carries the full opportunity cost of the transit. The rate on the screen is identical. The real cost is not.

Mileage and residual depreciation come next. Every mile driven during a relocation transit is a mile of value lost. Mileage-related depreciation on fleet passenger cars runs roughly $0.30 to $0.35 per mile, so a 1,000-mile relocation adds $300 to $350 in depreciation to that vehicle. A carrier-hauled car adds zero road miles. That gap matters most for vehicles approaching their remarketing threshold and for higher-value units, where the depreciation curve is steeper.

Fuel is the one real cost that disappears — because the renter pays it. This is the mechanism that makes $1/day viable at all. The traveler absorbs roughly $100 to $200 in fuel on a 1,000-mile trip, cost you would otherwise carry. Fair enough — but it’s worth being honest that this is the only one of the four costs the model actually eliminates for you, rather than hides from you.

Misplacement and timing risk is the most underappreciated. A relocation rental only works if a traveler wants your exact route in your exact window. On a high-demand corridor in peak season, that match is easy to find. On a thin lane or a narrow timing window, you may wait days or weeks — and while you wait, the car sits idle at the surplus location while the shortage at the destination deepens. A carrier move, by contrast, is dispatch-schedulable: you set a pickup date and a delivery window and plan around it.

There’s also a quieter difference in who carries the risk while the car is moving. A relocation traveler may be driving long distances through unfamiliar territory, sometimes under pressure to hit a drop deadline — a different exposure profile from a business renter on a short city loop. Standard rental insurance covers it, but the loss pattern on long, high-mileage relocation trips isn’t the same as on short urban rentals. A carrier move shifts that exposure onto the transporter’s commercial coverage: federal rules require auto haulers to carry significant public liability and cargo insurance, active from the moment the driver signs the bill of lading at pickup through the delivery signature, with the fleet operator — not a consumer — as the insured party. It’s a commercial claims process, not a consumer-facing one.

This is where the contrarian truth sits, and it’s worth stating plainly: the cheapest-looking reposition is the one without an invoice — and that’s exactly why it gets mispriced. The absence of a bill is not the absence of a cost. It’s the absence of visibility. Operators systematically underestimate the opportunity cost of relocation because they don’t measure utilization at the location level, so the number that should drive the decision never enters the math.

Carrier hauling carries the opposite profile: a visible cash cost and very little hidden cost. Understanding what drives that cash number — and what it buys you — is what makes the comparison fair.

Carrier rates are priced per vehicle and decline on a per-mile basis as distance grows. Short moves under 500 miles run higher per mile; long hauls past 1,500 miles run lower. For open transport of a standard passenger car, per-vehicle totals in current market conditions land roughly between $300 for short regional moves and $2,000-plus for cross-country runs.

The single most powerful lever you control is load consolidation. A standard open car carrier moves seven to nine vehicles, and the fixed costs of fuel, driver wages, and equipment get spread across every unit on the trailer. A fully loaded 9-car run can drop the per-vehicle cost to a fraction of a single-vehicle dispatch. The same trailer running half-empty distributes those fixed costs across three or four cars instead of nine, and the per-vehicle cost rises sharply.

The operational implication is direct: planned, batched repositioning during a predictable seasonal transition costs far less per vehicle than reactive, single-vehicle dispatching during or after the demand event. This is where larger fleet repositioning programs gain the most leverage.

We can put a number on the cost of reacting versus planning. Our own lane data shows June as the most expensive month for vehicle moves, averaging $1.20 per mile and $580.71 per move, compared with November’s $1.15 per mile and $517.75 per move. The summer peak isn’t expensive because the distance changed — it’s expensive because everyone moves at once, capacity is tight, and the planning window has closed.

That dynamic has been sharper than usual this year. This spring, our Illinois–South Florida corridor saw a larger rate increase than in prior years: diesel price increases stacked on top of the normal seasonal northbound premium as snowbird vehicles returned, pushing the lane above its typical spring level. When fuel and seasonality move in the same direction at the same time, the lane feels it twice.

Fuel itself is a structural part of carrier pricing, not an add-on. Surcharges are typically pegged to federal weekly diesel price indices and, in continental U.S. auto transport, are usually embedded directly in the per-mile rate rather than billed separately. The practical consequence for a fleet planner is rate volatility: spot pricing moves with diesel week to week, which makes a multi-month repositioning program hard to budget. Contracted carrier relationships often include rate-stability provisions — floor-and-ceiling arrangements that trade some upside and downside for planning certainty — which is worth more in a rising-cost market than in a falling one.

A carrier-hauled vehicle adds no road miles and accrues no additional wear in transit, and modern carriers protect vehicle condition in transit beyond mileage alone. For rental fleets — which typically cycle vehicles to remarketing at 20,000 to 40,000 miles, or 12 to 24 months, whichever comes first — every repositioning mile pushes a car closer to its exit threshold.

At $0.30 to $0.35 per mile in mileage depreciation, a 1,000-mile drive-based reposition adds $300 to $350 to a vehicle’s effective cost that a carrier move avoids entirely. The advantage is strongest for cars approaching their remarketing mileage, where each additional mile carries above-average residual impact, and for premium units with steeper depreciation curves. For a mid-life economy car, the effect is real but secondary. For a near-exit vehicle, it can decide the comparison on its own.

A carrier move comes with a date. The vehicle is unavailable during transit, but its arrival is predictable, so receiving stations can plan around a known arrival — staffing, reservations against incoming inventory, and accurate availability. Federal Hours of Service rules — the limits the FMCSA (Federal Motor Carrier Safety Administration, the agency that regulates commercial trucking) places on how long a driver can operate — cap daily progress at roughly 550 to 650 miles, which makes transit time itself predictable. A car dispatched from Illinois to South Florida, about 1,300 miles, typically arrives within a four-day window once it’s on a truck, against scheduled pickup and delivery windows.

A relocation rental offers that same certainty only if the renter’s schedule is fixed and verified — and in practice, travelers extend trips, change routes, and run late. You’re planning around a consumer’s calendar, not your own.

Carriers price the full round trip, not just the loaded leg. When a truck delivers into an over-demanded destination — Florida southbound in October, for example — the availability of a return load determines how aggressively the inbound rate is set. Lanes where inbound demand far exceeds outbound demand carry a premium, because the carrier has to absorb the cost of running empty on the way back. Industry deadhead averages 15–20% of total miles, and structurally imbalanced lanes push higher.

This creates a lever you can use. Repositioning in the direction the carrier is already fighting costs more; repositioning in the carrier’s preferred direction — adding to its backhaul — costs less. A fleet that can time some of its moves to ride with carrier flow, rather than against it, captures rate that an operator dispatching purely on its own calendar leaves on the table. The same Illinois–Florida corridor that commands a southbound premium in the fall rewards northbound loads in the spring, when carriers are hungry to fill trucks heading back.

One more factor is specific to right now. After nearly three years of soft rates, the auto transport market tightened materially heading into 2026 — carrier attrition has outpaced new entrants, capacity has contracted, and rates on popular routes have climbed by a double-digit percentage year over year. The practical implication is straightforward: advance scheduling and contracted capacity are worth more today than they were in the buyer’s market of recent years. Operators sourcing seasonal repositioning on the spot market now face both higher rates and longer waits than those who reserved capacity ahead of the season.

The decision is not relocation-versus-carrier as a standing preference. It’s a per-instance calculation, and you can model it on the back of an envelope.

Frame each side as a net cost from your perspective. The relocation rental’s net cost is its opportunity cost (market daily rate × transit days × expected utilization) plus mileage depreciation plus any timing-risk premium, minus the nominal revenue you collect. The carrier’s net cost is simply the per-vehicle rate plus any administrative cost — a direct cash outlay with little hidden behind it.

Watch what happens when you run a real example. A sedan needs to move 1,000 miles. The carrier rate is $700 for a partial load. The destination daily rate is $60. Origin utilization is 65% — below target. Expected relocation transit is five days.

Here, the relocation rental wins by about $190. The “expensive” carrier quote was the cheaper-looking number, but the relocation move was genuinely cheaper once you counted everything.

Now change one variable. Push origin utilization to 90% — the origin is actually short, and you’re repositioning preemptively — stretch transit to seven days, and assume a full-load carrier rate of $550. The relocation net cost becomes ($60 × 7 × 90%) + $320 − $7 = $691. The carrier now wins at $550. Nothing about the lane changed. The decision flipped on utilization and load.

That’s the core insight. Six variables move this decision, and they’re not equal. In rough order of sensitivity: origin utilization first, then transit days, then volume available for consolidation, then time-sensitivity at the destination, then where the vehicle sits in its lifecycle, and finally how much consumer relocation demand the lane actually has. Origin utilization dominates — which is precisely the number most operators don’t measure at the location level. Without it, the break-even is unknowable, and the relocation rental wins every argument it shouldn’t.

If the hidden-cost argument feels abstract, the one-way moving-truck market makes it concrete. Budget, Penske, and U-Haul all price one-way rentals directionally: the same origin-destination pair produces dramatically different prices depending on which way they need trucks to flow. Movers routinely document 2.5x to 3x price differences just by swapping the origin and destination ZIP codes.

That gap isn’t a service-quality difference. It’s the cost of fleet rebalancing, priced directly into the consumer transaction in plain view. It’s the same logic that drives relocation-rental discounting in car rental — only here, the operator’s inventory position is visible on the quote screen. The mechanism is identical; the moving-truck segment just doesn’t bother to hide it.

We’re an asset-based carrier — we own and operate our equipment rather than brokering loads to third parties — which gives us direct control over scheduling, quality, and the timing certainty that planned repositioning depends on. Our modern 9-car carriers protect vehicle condition in transit, and our real-time tracking lets receiving branches plan around a known arrival rather than a hopeful estimate. Every fleet client works with a named point of contact who plans batched moves in advance — which is exactly where carrier economics turn most favorable.

When does a relocation rental genuinely beat a carrier?

When origin utilization is below your fleet target, the lane has strong consumer travel demand, the move is short or low-volume, the vehicle isn’t near its remarketing threshold, and timing isn’t urgent. Under those conditions the opportunity cost is near zero and the relocation rental is the rational choice. The further you drift from that profile, the faster the math turns toward hauling.

How far in advance should we schedule seasonal repositioning?

Before the demand event, not during it. Reactive moves during a peak compete for scarce capacity at the highest rates of the year — our own data shows June moves running materially above November’s. Capacity has been tightening across 2026, which makes advance scheduling and contracted relationships more valuable than they were in the buyer’s market of recent years. The off-peak fall shoulder is usually the lowest-cost window for non-snowbird lanes.

Does carrier hauling really preserve enough residual value to matter?

It depends on the vehicle. For a mid-life economy car, the mileage saved is a secondary factor. For a unit approaching its remarketing threshold, or a premium vehicle with a steep depreciation curve, the $300-plus in mileage depreciation avoided on a 1,000-mile move can swing the decision by itself.

The reposition-or-haul question has no fixed answer, and any vendor who gives you one is selling rather than advising. It’s a per-instance calculation dominated by a single number — origin utilization — that most fleets don’t track location by location. Get that number right and the rest of the math falls into place. Skip it, and the relocation rental will keep winning arguments it should lose, because the cheapest-looking option is the one that never sends you a bill.

Before your next seasonal transition, pull utilization for each of your surplus origin locations and run the break-even, lane by lane, using your own daily rates and contracted carrier costs rather than industry averages. That single exercise will tell you where relocation rentals genuinely save money and where they’re quietly costing you more than a carrier would. For the lanes where hauling wins, line up capacity early — in a tightening 2026 market, the operators who plan ahead are the ones who get the rate and the date they want.

Stay informed on the latest news and insights from GB Cargo.